All Categories

Featured

Table of Contents

Misalignment can lead to unneeded costs or inexible financial obligation. A term loan provides a xed lump sum, repaid over a set period with predictable payments and a set rate. It's ideal for specic, one-time investments like devices, restorations, or acquisitions, and normally oers lower rate of interest, especially if secured. An organization line of credit is a revolving account with a limitation.

Navigating Digital Tax Laws with Smarter PaymentsIn short, term loans nance things (e.g., purchasing an oven), while lines of credit handle money circulation (e.g., covering a sluggish season). Lots of organizations benefit from using both for their intended function.

Consulting with an industrial lending professional before using can help clarify which structure makes one of the most sense for the specic usage of funds, the repayment timeline that ts your company's money ow, and whether a combination of both items much better serves your business's general nancing method. A well-prepared loan application does more than satisfy a list.

How to Optimising Digital Stock Systems Smartly

Incomplete or disorganized applications are one of the most common and most preventable factors for delays and denials. Getting the documentation right before you submit puts the application in the greatest possible position from the first day. The core documents most lending institutions require consist of individual and organization income tax return for the past 2 to 3 years, recent prot and loss declarations, a present balance sheet, service bank declarations for the previous three to six months, and a financial obligation schedule revealing existing commitments.

The more total and organized the bundle, the faster the underwriting process moves. Lenders highly value the Financial obligation Service Coverage Ratio (DSCR), which determines an organization's money ow against its current and asked for financial obligation obligations. A minimum DSCR of 1.25, suggesting $1.20 in operating earnings per $1.00 of financial obligation service, is generally looked for.

Understanding your DSCR ahead of time enables you to address shortages or customize the loan request. Beyond metrics, lenders need a specic, sensible loan purpose.

Key Pros of Modern SME Finance

The majority of conventional lending institutions require a minimum of two years in company, tidy income tax return, nancial declarations, and a clear explanation of how profits will be utilized, according to Small company Trends. Collecting these files before you begin the application, instead of assembling them under deadline pressure, minimizes errors and offers you a chance to capture potential concerns, such as disparities between tax returns and bank statements, before the loan provider does.

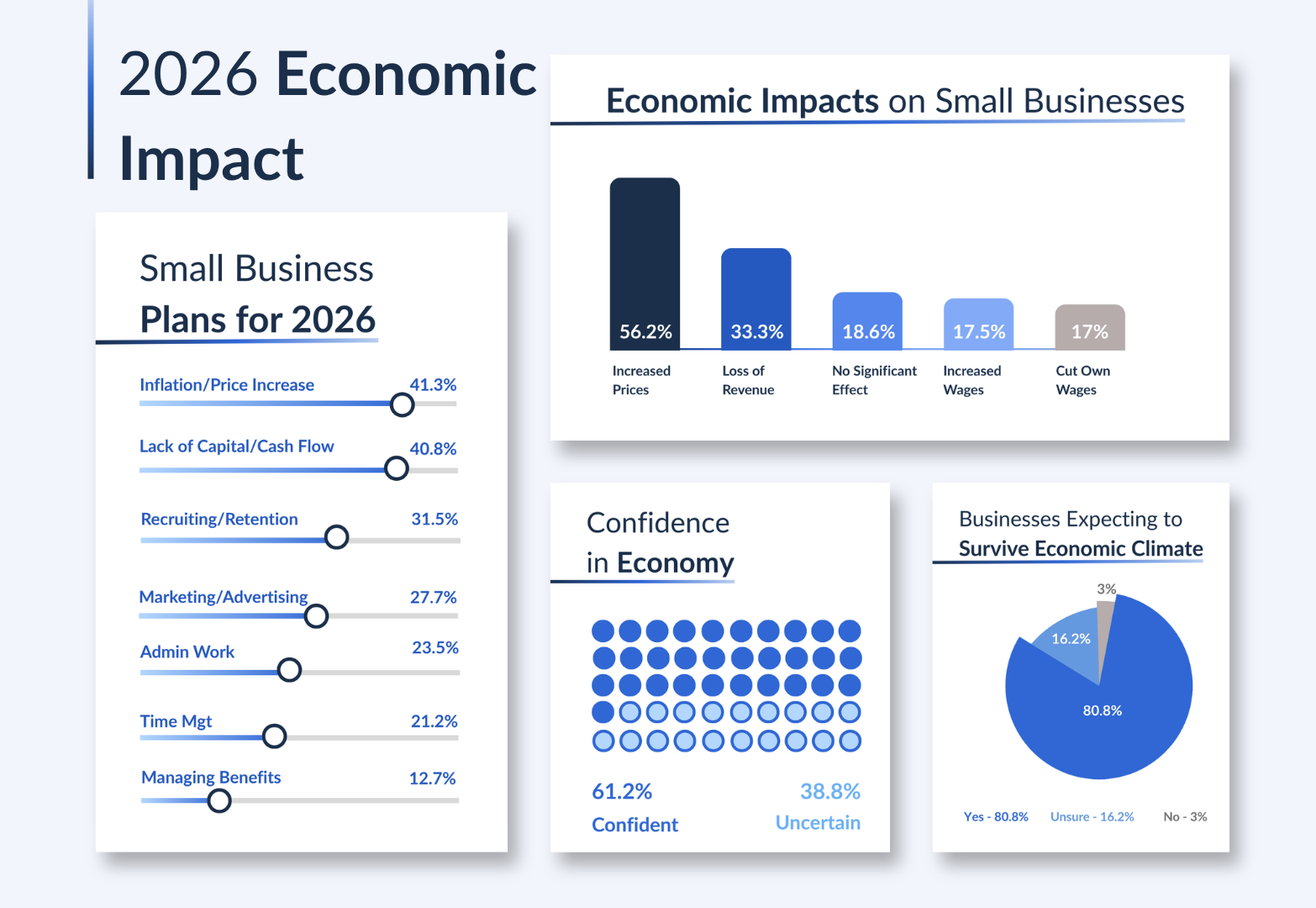

That means more than half of all applicants did not get fully moneyed. Comprehending why rejections occur and what lenders are really looking for offers company owners a concrete course to improving their chances before sending.

As covered in Section 4, debtor nancials account for approximately 68% of denial factors according to Federal Reserve lending data. Paying down existing responsibilities before using, or applying for a smaller sized amount that ts within existing cash ow capability, directly addresses this problem.

The Complete Modern Business Loan Approval Guide

A personal score listed below 650 signicantly narrows the swimming pool of lenders ready to approve an application, and listed below 600, it ends up being really dicult outside of alternative nancing channels with less beneficial terms. Services under two years old are not locked out of nancing entirely, however they typically require to rely on the owner's personal credit prole more greatly, provide more powerful security, or explore SBA programs developed for earlier-stage business. Insufficient or inconsistent paperwork rounds out the most typical rejection causes.

Lenders view disordered documents as a proxy for how business is handled. Resolving it before submission expenses absolutely nothing and gets rid of an easily avoidable barrier. The most common reasons rms were rejected or underfunded were weak nancials, insucient money ow to cover existing and new debt responsibilities, and credit rating concerns.

Building Long-Term Fiscal Stability

Not every business nancing need ts neatly into a term loan or credit line. For business prepared to get home, broaden physical operations, or invest in the automobiles and devices that drive revenue, specialized loan products oer structures better suited to those goals. iTHINK Financial oers both commercial real estate loans and lorry and equipment nancing for Florida and Georgia businesses at numerous stages of growth.

Business realty (CRE) loans are long-term nancing products secured by the home itself, generally used to acquire oce space, retail locations, storage facilities, medical centers, or mixed-use buildings. Terms, rates, and loan-to-value ratios vary based upon property type, service nancials, and the debtor's credit reliability. For organizations that want the benets of CRE nancing with a government-backed structure, the SBA 504 loan program deserves thinking about.

Florida First Capital Finance Corporation (FFCFC), which serves Alabama, Florida, and Georgia, is an SBA-authorized CDC that works along with loan providers like iTHINK Financial to structure 504 loans for qualifying businesses in the region. In addition to the 504 program, the SBA 7(a) program can likewise be utilized for commercial real estate and is typically a preferred choice due to its exibility in structure and more comprehensive use of profits.

iTHINK Financial's lorry loans and devices nancing through service financing services supplies nancing for both brand-new and secondhand business cars and devices, with terms structured around the property being nanced. This kind of nancing is especially relevant for companies in construction, logistics, landscaping, health care, and other asset-intensive markets common across Florida and Georgia.

Leveraging Smart Workforce Scheduling for Higher ROI

The SBA 504 and 7(a) programs dier signicantly. The 7(a) is more comprehensive, covering operating capital, devices, real estate, and financial obligation renancing. The 504 is narrower, focusing on xed properties like property and major devices, however oering greater loan amounts and lower down payments for those uses. For Florida or Georgia organizations acquiring property or significant equipment, the 504 typically provides much better terms than a traditional CRE or 7(a) loan.

SBA loan timelines can differ from a couple of weeks to a couple of months based on the loan provider, loan quantity, and general application completeness. Among the most eective ways to avoid hold-ups is to send a fully total application upfront, consisting of tax returns, nancial declarations, an organization strategy, and personal nancial statements.

{kind=link}

Latest Posts

Meeting Updated Business Loan Criteria in 2026

Mastering Retail Inventory Management to Lower Costs

How Operational Automation Drives Long-term Financial Sustainability